1 of 5

1 of 5

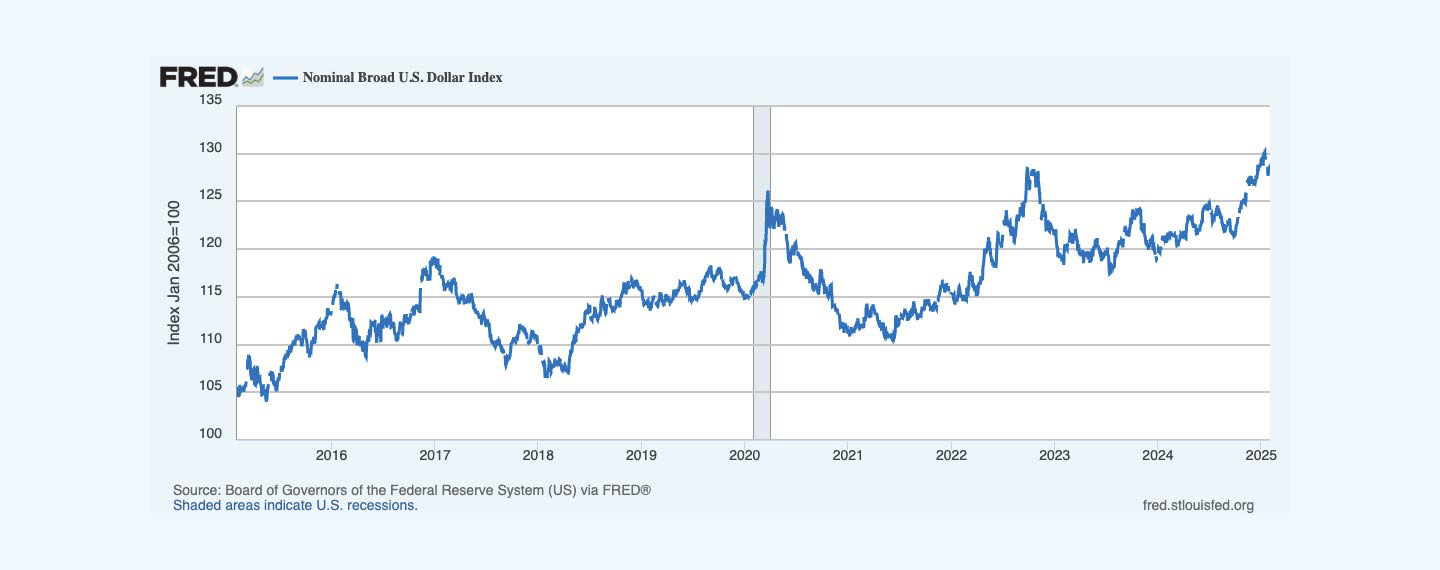

Studies that surprisingly failed to show much impact on company stocks when currencies move collectively led to what’s known as the “exchange-rate exposure puzzle.” A recent study, availing itself of more detailed per-company data, suggests:

2 of 5

2 of 5

What’s worse for today’s economy in India — being an area over which the British, ending in 1947, exerted direct control or an area where the British ruled indirectly through Indian officials?

3 of 5

3 of 5

In China, giving citizens a say in local budgeting decisions:

4 of 5

4 of 5

The Pacific Palisades and Altadena fires were devastating for residents in those areas. A working paper that examines past major fires suggests:

5 of 5

5 of 5

The FDIC insurance limit per deposit account is $250,000, but a little-examined expansion, known as reciprocal deposits, allows your bank to hand off amounts over that limit to other banks, affording depositors protection of many multiples of the limit. Great for bank customers. The loser from this program appears to be: