Their level of technology and services makes up for it; it’s vice versa with little banks

After a near 15-year hiatus, the Federal Reserve’s return to tighter monetary policy beginning in early 2022, in the name of taming inflation, has roiled the banking industry.

The failure of two midsized banks in 2023 — and concerns their problems might develop into an industrywide run on deposits — was one result of the rapid rate hikes.

Opt In to the Review Monthly Email Update.

Rising short-term interest rates also reignited the ability of consumers to earn a decent return on cash. That’s created renewed competition for banks, as money market mutual funds offered through fund complexes are now offering superior rates. Since early 2022, total bank deposits have dipped by $1 trillion (to a still staggering $17 trillion) and money market mutual fund assets have grown by about $1 trillion.

A Trade-Off at Large Banks?

A working paper by Stockholm School of Economics’ Adrien d’Avernas, UCLA Anderson’s Andrea L. Eisfeldt, University of Illinois’ Can Huang, and UC Berkeley’s Richard Stanton and Nancy Wallace offers a fresh explanation for why small banks likely suffer more than big ones during this change in the deposit gathering business.

The researchers present evidence that large banks cater to customers who are less concerned about what they earn on cash accounts, while customers of small banks are more sensitive to what they can earn, effectively requiring the smaller banks to offer higher deposit rates.

Given that customers of large banks typically are higher-income households in urban areas, the standard theory is that they are more financially sophisticated. That would suggest that big-bank customers should be more sensitive to earning low returns, not less sensitive.

So what gives?

The research suggests customers of big banks seem to accept, or perhaps embrace, a trade-off: In return for valued enhanced liquidity services — including techy services like online and app banking, as well as copious ATMs — customers of large banks on average accept lower deposit rates. Meanwhile, small banks are notoriously short on tech that eases customer use/access, and with less cash-like deposits they are left to compete for customers by offering more competitive deposit rates.

This research extends the conversation about why large bank customers are less rate sensitive. Long presented as a function of the sheer market dominance of big banks — they can set the market rate because they are the market — this new analysis suggests it is more of a symbiotic relationship between big banks and their target customers: The bank invests in technology to provide services that its target customer values. In return, the customer, however tacitly, absorbs some of that cost by typically accepting lower deposit rates rather than moving their cash somewhere it can earn more.

This observation illuminates a potentially important element in parsing bank valuations and bank financial stability as the Fed’s zero-rate interest policy is now in the rearview mirror. It suggests that large banks feel less pressure to narrow their spreads — the difference between what they earn on loans and other assets and what they pay out on depositors to fund those assets — than smaller banks that bear more risk customers will indeed shop on rates.

“Small banks may be more vulnerable in a tightening environment because their customers are more sensitive to deposit rate changes and because they need to incur higher funding costs by offering higher rates to retain deposits,” the researchers write.

Deposit Volatility as a Function of Bank Size

The researchers used bank deposit and rate data spanning 2001 to 2019. The 14 largest U.S. banks heading into 2009 constitute their universe of big banks. As of 2019 these 14 banks held 55% of total U.S. deposits. They then drill down to county-level deposit rates offered by big banks versus smaller banks. While they have more than 3,000 counties to work with, they combine less-populous counties into clusters; they end up with 1,330 such groupings to analyze.

They then build their thesis from related empirical data:

Bank Size as Driver of Customer Base. The research asserts that big banks seek out markets where liquidity services are highly valued. That typically means large urban areas, which on average are younger and have higher household income than less-urban areas. The red areas in the map below are where the branches of big banks operate, the darker the shade of the green the more populous an area. The red dominates in coastal and denser counties.

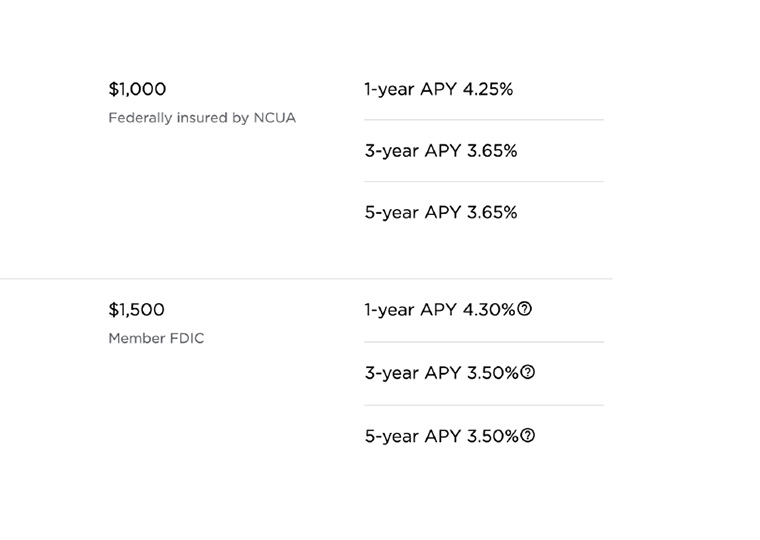

Bank Size Drives Rates. The researchers focused on three popular deposit products:

A $10,000, 12-month CD

A $25,000 bank money market deposit account

And savings accounts with balances below $2,500

As shown in the graphs, small banks typically offer higher rates than the 14 big banks. (Note: The researchers also establish that big banks do not offer localized rates for their branch operations; they instead rely on “uniform” rates offered to all customers.)

Interestingly, the researchers did a separate analysis of small banks in counties where big banks also operate. They found that the interest rates offered were lower than the average interest rates for all small banks. That is, when small banks operate in markets where depositors value other aspects of deposits besides the deposit rate, they also offer lower rates.

Bank Size Is the Largest Driver of Rate Differences. Because certain-sized banks target certain demographics and thus locations, bank size in this research also takes into account demographic differences. The researchers estimate that bank size explains 21% of the variance in CD rates, 11% of the money market rate variance and more than 15% of the savings rate difference between big and small banks.

Small Banks More Exposed to Customer Reaction to Rate Changes. Having parsed these significant differences between large and small bank market dynamics, the researchers model out the extent to which bank size correlates to customer sensitivity to deposit rates.

They confirm what is suggested by their foundational findings about operational differences based on bank size: Smaller banks face more demand elasticity.

In their model, when deposit spreads — the difference between the Fed Funds rate and the rate a bank pays out in deposits — widen by 1%, deposits decrease an average of 0.41% at small banks, while deposits at large banks fall 0.26%. The median elasticity for small banks is approximately four times that of large banks.

Given the centrality of deposits to bank operations, these findings suggest potentially more stress for smaller banks. The research also provides a more nuanced explanation for how a dozen or so big banks that dominate the market are able to pay less competitive rates on demand deposits.

“(M)uch of the variation in deposit pricing behavior across banks may be due to variation in (customer) preferences and technologies as opposed to being driven purely by pricing power derived from the large observed degree of concentration in the banking industry,” the researchers conclude.

Featured Faculty

-

Andrea L. Eisfeldt

Laurence D. and Lori W. Fink Endowed Chair in Finance and Professor of Finance

About the Research

D’Avernas, A., Eisfeldt A.L., Huang, C., Stanton, R., & Wallace, N. (2023). The Deposit Business at Large vs. Small Banks. doi: 10.3386/w31865