Reminding people that payroll taxes will keep flowing in — even after the trust funds hit zero — helps them understand benefits won't disappear

A widespread misperception — that Social Security is going broke — could be substantially corrected by emphasizing how money continuously flows into the system, rather than focusing on the dwindling balance of the system’s trust funds, explains forthcoming research in the Journal of Experimental Psychology: General, by UCLA Anderson’s Megan E. Weber, a Ph.D. student, Stephen A. Spiller and Hal E. Hershfield, and Cornell’s Suzanne B. Shu.

Social Security is a very popular program — that, these days, is also anxiety-inducing. A recent survey by the Transamerica Center for Retirement Studies found that more than 70% of working Americans are concerned that, when they are ready to retire, Social Security won’t be around for them.

That fear is understandable given countless headlines warning that the program will soon “run out” of money, “go broke” and faces imminent “insolvency.”

While the retirement system’s financial situation is serious, it is not nearly as catastrophic as the headlines imply. Social Security has a cash flow problem but isn’t going bankrupt. Social Security is generally a pay-as-you-go program, meaning that payroll deductions from currently working people are used to fund retirement benefit checks cut each month. In some eras, payroll deductions collectively exceeded benefits due, and the trust funds collected and stored this excess. In other times, like recently, deductions don’t entirely cover benefit payments, and the funds are drawn down to cover the shortfall.

Now, absent congressional reform, the funds would be exhausted and, beginning in 2035, incoming payroll deductions would be able to cover 75%-80% of benefits payments. Not great, but a whole lot better than the $0 implied in headlines.

Stocks Vs. Flows

Across multiple experiments, the researchers show that Americans’ fear that Social Security will stop paying any benefit may be partly rooted in what the authors call “inflow neglect” — forgetting about a key mechanism in how the program works. Millions of workers will continue paying into the system in 2035 and beyond.

Focusing on the “stock” of the dwindling trust funds, as opposed to the “flows” of payroll deductions, is akin to freaking out because one’s bank account is nearing zero, but failing to realize that a paycheck from your steady job hits the account tomorrow.

The researchers find that simple interventions that increase awareness of the continuing inflow of payroll taxes into the system noticeably decreases the share of people who think payments will go to zero.

This research, partially funded by the Social Security Administration, builds on earlier work Spiller collaborated on that exposed how design choices made when creating data visualizations influence a viewer’s judgment.

Two Graphs

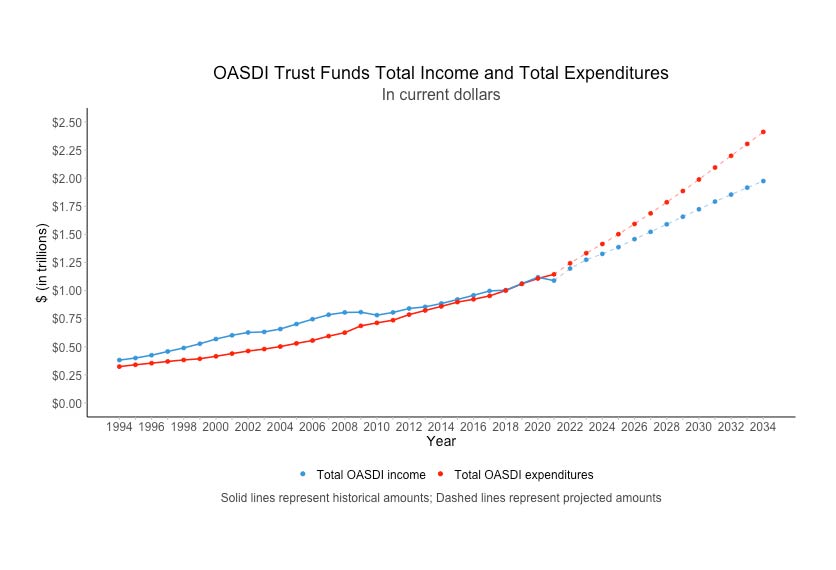

In one experiment participants were shown a graph of the trust funds’ balance declining over time toward zero.

When asked what would happen once the trust funds hit zero, 64% of participants incorrectly responded that benefits would stop entirely.

Another group was shown a different presentation: Instead of the declining trust funds balance, the graph displayed the flows — inflows from ongoing payroll tax collection, and benefit outflows over time. As shown below, this dramatically shifts the focus to the fact there is a funding gap, not a bankrupt system.

In this group, 56% of participants assumed benefits would drop to zero, a meaningful reduction in misunderstanding, if still a troubling majority.

Researchers Made Further Progress

Another experiment nudged participants to focus on the continuing flows by asking them if they thought payroll tax collection would continue even after the trust funds were depleted, and how they thought those payroll taxes would be used. About 90% of participants correctly answered that payroll tax inflows don’t stop in 2035.

When participants were asked about the fate of future benefits before being prompted to think about continuing inflows, 66% mistakenly believed benefits would fall to zero. But when another group was first guided to think about the role of continuing payroll tax inflows — and then asked about future benefits — only around 40% believed benefits would completely disappear.

Granted, 40% answering incorrectly is still problematic, but the fact that a simple prompt reduced misunderstanding by 26 percentage points is a significant improvement.

And the participants who “reflected” on future flows before thinking about future benefit levels came in with the highest estimate of what those benefits would be, compared with participants who answered the flows question after. Yet across multiple experiments, participants are unduly pessimistic, estimating future benefit levels would be reduced to just 40% or less of current benefits, not 75%-80% in 2035 of benefits even if Congress doesn’t enact reforms.

That would seem to be another opportunity for crafting better communication to tamp down costly misperceptions.

An AARP survey in summer 2025 found that nearly half of people who recently opted to start collecting Social Security earlier than they originally planned — or now plan to take it earlier — cited concerns that the program is running out of money. That comes at a tangible cost, as anyone who chooses to start their benefit early — there is an eight-year claiming window beginning at age 62 — locks in a permanently reduced payout. Hershfield, Shu and Spiller collaborated in earlier research on how people might be persuaded to put off claiming benefits so as to increase rest-of-life payments.

Today’s maximum monthly payout at age 62 is $2,969 versus $5,181 at age 70. And according to Pew Research Center analysis from 2022, for 63% of people receiving social security, the payout accounted for at least 50% of their total personal income. That’s 38 million Americans in 2022.

Encouraging more people to focus on the continuing inflow of payroll tax into the system in 2035 and beyond, and how that will enable the majority of benefits to continue, might help reduce the urge to claim earlier. It might also spur a more constructive conversation between voters and their legislative representatives: Fixing a 20% cash flow gap is a lot more doable than thinking the challenge is to replace a completely bankrupt system.

Featured Faculty

-

Megan Weber

Behavioral Decision Making, Ph.D. candidate

-

Stephen Spiller

Professor of Marketing and Behavioral Decision Making

-

Hal Hershfield

Professor of Marketing and Behavioral Decision Making

-

Suzanne Shu

Professor Emeritus of Marketing

About the Research

Weber, M.E., Spiller, S.A., Hershfield, H.E., & Shu, S.B. (in press). Inflow Neglect: Forecasting Failures After Stocks Run Out. Journal of Experimental Psychology: General.